Introduction

Extreme concentrations of wealth are often justified as the fair reward for bold risk-taking. This report asks what “risk” really means when the investor is a billionaire—and who actually bears it. We begin by examining how limited liability, moral hazard, and state backstops cap elite losses while shifting catastrophic downside onto workers, taxpayers, and communities. We then trace how ultra‑wealthy investors recode risk through leverage, tax deferral, and carefully structured “skin in the game.” Next, we show how SPVs and bankruptcy law engineer downside for others. Finally, we challenge the moral narrative that equates billionaire “risk” with ordinary people’s existential stakes.

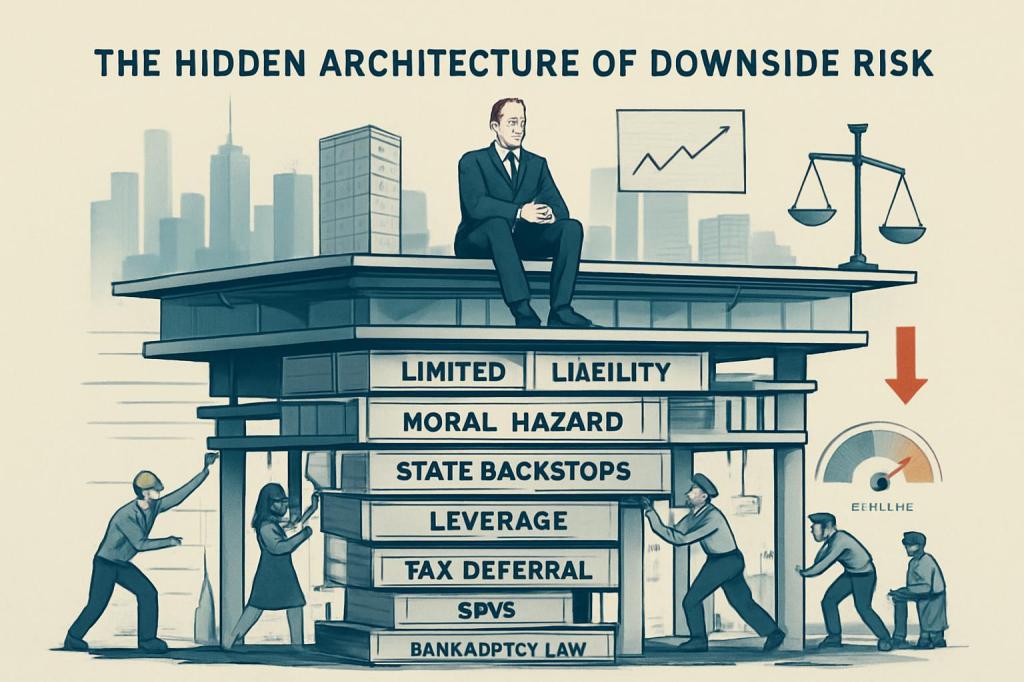

Extreme concentrations of wealth are routinely defended as the payoff for shouldering extraordinary risk. Across corporate law, financial engineering, and tax strategy, the materials here show something different: the ultra‑rich and their entities systematically reconstruct risk so that large, leveraged bets deliver mostly upside to insiders while shifting or capping their own downside. The result is not the absence of risk in the system but its redirection—onto workers, small investors, “non‑adjusting” creditors, and taxpayers.

At the core is limited liability, which functions less as a neutral legal convenience than as a structural reshaping of incentives. When both managers and corporations know that their personal and entity‑level downside is capped—by limited liability, bankruptcy discharge, and exemptions—they have weaker reasons to spend on loss prevention or to restrain tail risks, especially where prevention effort is hard to observe and contract on [1]. Dynamic moral hazard models show that when potential losses can exceed available assets, actors rationally under‑invest in safety; future sanctions like downsizing or liquidation may discipline managers but can be ex post inefficient, destroying jobs and community wealth without making decision‑makers absorb the full costs of their bets [1]. Empirical work on capital structure confirms this: firms tend to choose more leverage when they can externalize some of the downside, turning debt into a tool for amplifying returns precisely because someone else is left holding the bag when things break [2].

Legal doctrines magnify this pattern. Limited liability is explicitly designed to cap investor losses and encourage capital formation, but it also allows systematic externalization of harms—onto tort victims, small trade creditors, and tax authorities—who cannot contract around the risk [3][6]. This is most troubling when key hazards are “known unknowns”: insiders know that serious residual risks exist (to health, environment, or financial stability) but their scale and likelihood remain opaque to regulators and the public [3]. In such settings, standard risk‑management tools—capital requirements, mandated insurance—only partially work, because near‑misses and small private losses accumulate in the shadows rather than triggering visible market or regulatory correction [3].

Government backstops convert this structural insulation into explicit public guarantees. Nationalizations, debt assumptions, and emergency bailouts allow private actors to keep the upside from risky strategies while offloading catastrophic downside onto the state [4]. Unlike conventional insurance, where riskier behavior is disciplined over time through higher premiums, federal rescues often impose no commensurate future cost on those who benefited from the bailouts [4]. This creates a standing invitation to speculate with the public safety net as the ultimate absorber of loss.

Around these legal foundations, modern financial engineering further insulates billionaire‑controlled capital. Private equity provides a vivid case. High‑net‑worth investors are drawn into PE funds by promises of superior, uncorrelated returns, but the environment is structurally opaque: portfolio company values are “marked to model,” disclosures are thin, and reporting is irregular [1]. High leverage means that adverse shocks—rate rises, credit tightening, operational setbacks—translate into outsized bankruptcy risk, and PE‑backed companies make up a disproportionate share of large corporate failures [1]. While sponsors and principals benefit from fees and asymmetric upside, losses cascade onto employees, unsecured creditors, and communities when over‑leveraged firms implode.

Special purpose vehicles (SPVs) and securitization structures are marketed as neutral tools for “isolating” risk, yet they often function as precise mechanisms for reallocating it. By inserting an SPV between the originator and investors, securitizations create a legally separate entity that formally owns the assets; those assets are then insulated from the originator’s bankruptcy estate, a design described as “bankruptcy‑remote” [2]. This lowers funding costs for sophisticated sponsors and investors, but thins the asset pool available to other creditors if the originator fails. In practice, investigations frequently reveal a gap between formal structure and economic reality: assets never properly transferred, collateral quality overstated, cash flows diverted, or multiple lenders relying on the same collateral under different SPVs [4]. Rating agencies often base evaluations primarily on the SPV’s apparent asset quality and structural protections, further decoupling investor risk from the underlying operating business’s true solvency and leaving less protected stakeholders to absorb residual losses [5].

Layered over this is the baseline of corporate and personal limited liability. Equity is formally the residual claimant, supposed to bear the last losses in exchange for control and upside [3]. But the widespread use of SPVs, securitization safe harbors, and multi‑entity structures allows value to be rerouted before insolvency rules apply. Private equity sponsors and billionaire principals can enjoy fee income and upside participation while placing operating risk inside thinly capitalized entities; if catastrophic claims arrive, personal bankruptcy and exemption rules operate as an additional “insurance layer,” allowing them to discharge obligations that exceed what they are willing to put at stake [6]. Scholars describe this as a “massive, regressive cross‑subsidy,” with under‑compensated creditors, workers, and the public financing the liability shield enjoyed by capital owners [6].

On the surface, these arrangements showcase the wealthy as archetypal risk‑takers. Yet their direct financial behavior reveals an effort not to embrace risk so much as to transform it into controlled, often subsidized exposure. A signature pattern is the “buy, borrow, hold” model: rather than selling appreciated assets and realizing taxable gains, billionaires accumulate wealth as unrealized appreciation, then borrow against those assets to fund consumption and further investment [1]. Because investment gains are untaxed until realized, and borrowing costs can be lower than expected after‑tax asset returns, leverage becomes a tax‑advantaged liquidity and reinvestment tool instead of a simple amplifier of volatility. This allows the ultra‑rich to maintain high exposure to diversified, appreciating assets while smoothing cash flow and minimizing realized tax, significantly altering their effective downside profile.

Sophisticated private investors use a similar logic when leveraging stable, cash‑flowing assets to acquire new ones. The point is not merely to “bet bigger” with borrowed money, but to stack multiple compounding engines while ring‑fencing failure modes: separating idiosyncratic operational risk (a specific business failing) from balance‑sheet liquidity risk (margin calls, forced sales) [2]. With diversified collateral, low personal guarantees, and access to refinancing, a wealthy investor’s probability of ruin is dramatically lower than that of a small, undiversified borrower—even when headline leverage ratios look similar.

Institutional evidence from private equity general partners (GPs) clarifies how true “skin in the game” works. When GP co‑investment is measured relative to their personal wealth, higher personal exposure is associated with less risky portfolio company selection overall, even though those portfolio firms themselves may carry high leverage; total equity risk at the GP level falls as their personal stake rises [3]. This suggests that where decision‑makers genuinely internalize downside, they choose safer deals and design capital structures more carefully. It also underscores how, in many real‑world settings, billionaire sponsors and managers use entity shields and investor capital to avoid bearing this kind of personal risk in the first place.

These financial and legal architectures interact with the deeper economic forces that generate extreme fortunes—especially network externalities and winner‑take‑all dynamics in digital and platform markets. Many tech and platform billionaires draw their wealth from structures where value increases simply because many people coordinate on the same product or platform. These network externalities exist independently of any one entrepreneur; the market selects a narrow set of “winners” among many similarly capable competitors, assigning outsized gains to those best positioned to capture the positive feedback loop [1]. Effort, talent, and some risk‑taking determine who wins, but not the scale of the windfall.

This undercuts standard moral narratives about risk and reward in two ways. First, the stakes faced by the ultra‑rich and by ordinary people are incommensurable. A billionaire can lose hundreds of millions in a failed venture and still retain secure housing, healthcare, education for their children, and high social status. A small business owner, indebted graduate, or gig worker can face bankruptcy, homelessness, and long‑term exclusion from credit after a single failed risk. Legally and financially, both may be said to have “taken a risk,” but the lived consequences—what is actually at stake—are qualitatively different.

Second, if extreme wealth is disproportionately driven by structural features like network externalities and by institutionalized downside protection, then the enormous gap between billionaire outcomes and those of “near‑miss” peers cannot be justified by appeal to proportional contribution or personal risk exposure. Markets in such sectors do not reward moral desert; they distribute rents according to structural position, path dependence, and the ability to exploit existing externalities [1]. On a meritocratic view centered on contribution and fair reward, this weakens the argument that extreme fortunes are earned as just compensation for risk.

Taken together, the evidence suggests that billionaire “risk-taking” is largely about designing environments in which genuine personal exposure to ruin is minimal, while upside from large, leveraged, and sometimes socially hazardous bets is preserved. Limited liability, bankruptcy law, SPVs, securitization, and “buy, borrow, hold” tax strategies collectively reallocate risk rather than eliminate it. What appears as bold entrepreneurial courage at the top often rests on a finely tuned insulation from loss—paid for, directly or indirectly, by those with the least choice and the most to lose.

Conclusion

Across these sections, a common pattern emerges: billionaire “risk-taking” is carefully engineered to bound personal downside while leaving others exposed. Limited liability, bankruptcy law, SPVs, and securitizations redirect catastrophic losses to workers, creditors, and taxpayers, even as legal rhetoric portrays equity as bearing the residual risk. At the top of this structure, the ultra‑wealthy further reshape risk through leverage, tax deferral, and balance‑sheet design so that volatility becomes optionality, not existential threat. Combined with winner‑takes‑all dynamics and network externalities, this architecture shows that extreme fortunes rest less on bearing risk than on orchestrating who must bear it instead.

Sources

[1] https://www.fmg.ac.uk/sites/default/files/2020-08/large-risks.pdf

[2] https://www.nber.org/system/files/working_papers/w1145/w1145.pdf

[3] https://corpgov.law.harvard.edu/2018/03/04/limited-liability-and-the-known-unknown

[4] https://scholarship.law.ufl.edu/cgi/viewcontent.cgi?referer=&httpsredir=1&article=1088&context=flr

[5] https://www.oxfamamerica.org/explore/stories/top-5-ways-billionaires-are-bad-for-the-economy

[6] https://www.bny.com/wealth/global/en/insights/adopting-a-billionaire-mindset-with-borrowing.html

[7] https://www.linkedin.com/posts/walkerdeibel_a-private-banker-once-told-me-there-are-3-activity-7430642662094913536-SX8P

[8] https://www.dbj.jp/ricf/pdf/research/DBJ_DP_1801.pdf

[9] https://www.citrincooperman.com/In-Focus-Resource-Center/Private-Equity-for-High-Net-Worth-Individuals-Opportunities-and-Risks-Explained

[10] https://nyujlpp.org/wp-content/uploads/2016/01/Kirshner-Bankruptcy-Safe-Habor-in-Light-of-Government-Bailouts-18nyujlpp795.pdf

[11] https://scholarship.law.cornell.edu/cgi/viewcontent.cgi?article=3518&context=clr

[12] https://www.alvarezandmarsal.com/thought-leadership/the-hidden-risks-inside-spv-and-nontraditional-financing-structures-what-every-board-and-lender-should-know

[13] https://www.hofstralawreview.org/wp-content/uploads/2013/02/40-1-Pearce-Lipin-Hofstra-Law-Review.pdf

[14] https://www.abi.org/feed-item/private-equitys-abuse-of-limited-liability

[15] Oxfam. Extreme Wealth Is Not Merited. https://www-cdn.oxfam.org/s3fs-public/file_attachments/dp-extreme-wealth-is-not-merited-241115-en.pdf

Written by the Spirit of ’76 AI Research Assistant

Leave a comment